In 2025, Nigeria's embedded finance market will reach $4.34 billion. That figure, drawn from ResearchAndMarkets' latest analysis, is not just a statistic. It is evidence of a fundamental shift in how financial services are delivered across Africa, one where the line between "fintech company" and "everything else" is becoming increasingly blurred.

Behind this growth is a quiet revolution. A Lagos-based logistics startup now offers merchants real-time settlements and business insurance, eliminating the need to visit a bank. A Nairobi e-commerce platform provides instant credit at checkout, turning browsers into buyers.

A ride-hailing driver in Accra receives fare payments and accesses short-term loans through the same app that powers their daily work.

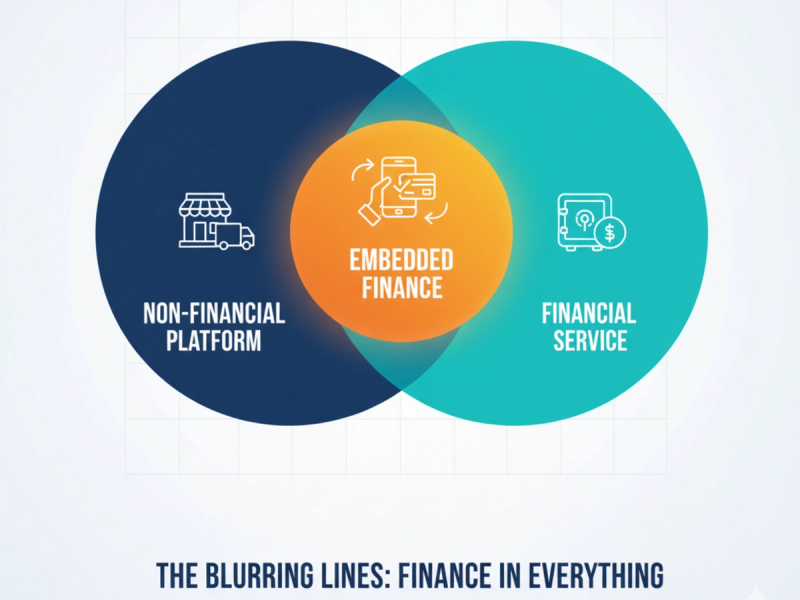

These are not isolated innovations. They are symptoms of embedded finance, the integration of financial services directly into non-financial platforms, transforming African commerce in ways that extend far beyond simple payment processing.

The Numbers Tell a Transformation Story

The growth trajectory of embedded finance in Africa has moved from promising to undeniable. Nigeria's market alone has experienced a compound annual growth rate of 12.2% between 2021 and 2025, according to ResearchAndMarkets.

By 2030, the market is projected to reach $5.55 billion. South Africa, the continent's most mature market, is expected to hit $2.92 billion in 2025, growing at 11.1% annually after achieving a 16% CAGR during 2021-2025.

Globally, embedded finance is set to grow beyond $228 billion by 2028, according to Juniper Research. Africa, despite starting from a smaller base, is showing adoption patterns that suggest it could capture a disproportionate share of this growth relative to its current financial services penetration.

However, these aggregate numbers obscure the more interesting story: where embedded finance is actually appearing and why it matters.

The Shift: Every Platform Becomes Financial Infrastructure

Walk through a typical day for millions of Africans, and embedded finance is everywhere, even if they don't recognize it by that name.

A market woman in Ojuelegba, Lagos, Nigeria, uses a retail app not just to track inventory but to access micro-working capital when stock runs low. The credit decision happens instantly, based on her transaction history within the app. She never visits a bank or fills out a loan application. The financial service is embedded in the commercial tool she already uses daily.

A university student in Kampala books accommodation through a property platform that offers payment plans allowing them to spread rent across the semester. The platform partners with a financial services provider in the background, but the student experiences it as a natural feature of the platform itself.

These examples share a common pattern: financial services appearing at the exact moment they're needed, within the context where they're needed, delivered by platforms that are not primarily financial institutions.

This is embedded finance in practice, and it is fundamentally different from both traditional banking and standalone fintech apps.

The Infrastructure Behind the Invisibility

For embedded finance to work seamlessly, sophisticated infrastructure must operate invisibly in the background. This is where companies like Zeeh, Paystack, OnePipe, and others have become critical enablers.

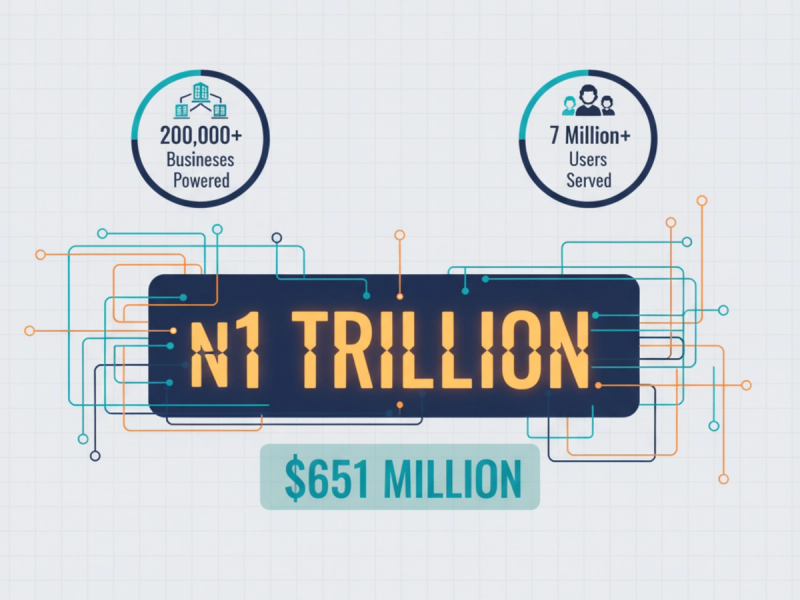

Paystack, which now powers over 200,000 businesses, processed ₦1 trillion in transactions in July 2024 alone, a number that would have been unthinkable just a few years ago. Zeeh, which builds open banking APIs, has handled over hundreds of thousands of transactions and serves more than 7 million users across Africa and the world.

OnePipe has turned its technology into a gateway for banks-as-a-service, allowing businesses to embed account creation, lending, and payments directly into their platforms through partnerships with Nigerian banks such as Fidelity and Access Bank.

This infrastructure layer is what makes it possible for a ride-hailing company to offer driver financing or an e-commerce platform to provide instant checkout credit. The platforms themselves don't become banks; they integrate with infrastructure providers who handle the complex regulatory, technical, and risk management requirements of financial services.

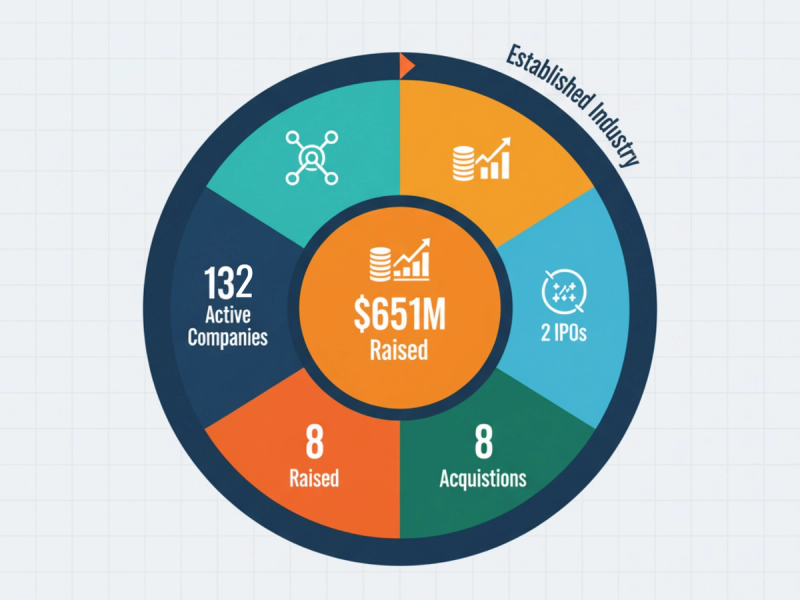

According to Tracxn data, Africa now has 132 active embedded finance companies as of July 2025, collectively raising $651 million in funding. The sector has seen eight acquisitions and two IPOs, suggesting it is maturing from an experimental stage to an established industry segment.

The Five Verticals Reshaping Commerce

Embedded finance in Africa isn't monolithic; it manifests differently across five distinct verticals, each with its own growth dynamics and use cases.

Embedded Payments: The Foundation

Embedded payments represent the most mature and widely adopted form of embedded finance in Africa. This is where Paystack and Flutterwave first demonstrated that financial services could be seamlessly integrated into e-commerce, logistics, and retail platforms.

The payments vertical includes not just checkout functionality but also payroll services embedded in HR platforms, subscription billing integrated into SaaS products, and settlement services built into marketplace platforms.

Africa's e-commerce sector, expected to reach $56 billion by 2026, provides massive growth potential for embedded payments as more transactions move online and payment infrastructure becomes more sophisticated.

Embedded Lending: Closing the Credit Gap

Perhaps the most transformative vertical is embedded lending, offering credit at the exact moment a customer needs it, within the platform where they're already transacting.

Buy-now-pay-later (BNPL) solutions have gained significant traction. Various fintech companies have introduced BNPL options, allowing consumers to purchase goods and pay in installments, with the embedded lending segment alone expected to reach $1.62 billion in Nigeria by 2025.

The opportunity is particularly significant given Africa's credit access challenge. Less than 6% of Nigeria's adult population accesses regulated credit despite high demand, according to Businessday analysis. Embedded lending reaches customers where traditional banks cannot.

Retailers like SLOT now offer device financing, and platforms like Checkout by Credit Direct have plugged into e-commerce sites, but these remain early examples of what could become much more pervasive.

Embedded Insurance: Protection When It Matters

Embedded insurance integrates coverage into relevant transactions, such as travel insurance at flight booking, device insurance at electronics purchase, or delivery protection at checkout.

This model addresses Africa's insurance penetration problem (historically very low) by making insurance contextual rather than requiring separate purchase decisions. When insurance appears as a natural option during a transaction, adoption rates increase dramatically compared to standalone insurance marketing.

The embedded insurance segment is still nascent in most African markets but shows strong growth potential as platforms recognize insurance as both a customer service enhancement and revenue opportunity.

Embedded Banking: Accounts Without Banks

Embedded banking enables platforms to offer account creation, money storage, and basic banking services without customers needing to visit physical bank branches or download separate banking apps.

Payment Service Banks, including nine Payment Service Banks, Hope PSB, MoneyMaster, MOMO, and SmartCash, are plugging into the same infrastructure that fintech entities built, blurring the lines between banks, telcos, and fintech startups.

This is particularly powerful for financial inclusion, reaching populations that traditional banks found economically unviable to serve through brick-and-mortar infrastructure.

Embedded Wealth: Democratizing Investment

The emerging fifth vertical involves embedding investment and savings products into platforms where people already manage money or make financial decisions.

This includes microsavings features in payment apps, investment options integrated into financial management tools, and retirement planning built into payroll platforms.

While less developed than other verticals in Africa, embedded wealth represents a significant long-term opportunity as middle-class populations grow and wealth accumulation becomes a priority for more Africans.

The Regional Dynamics

Embedded finance adoption across Africa is not uniform; it shows distinct regional patterns based on infrastructure maturity, regulatory frameworks, and market dynamics.

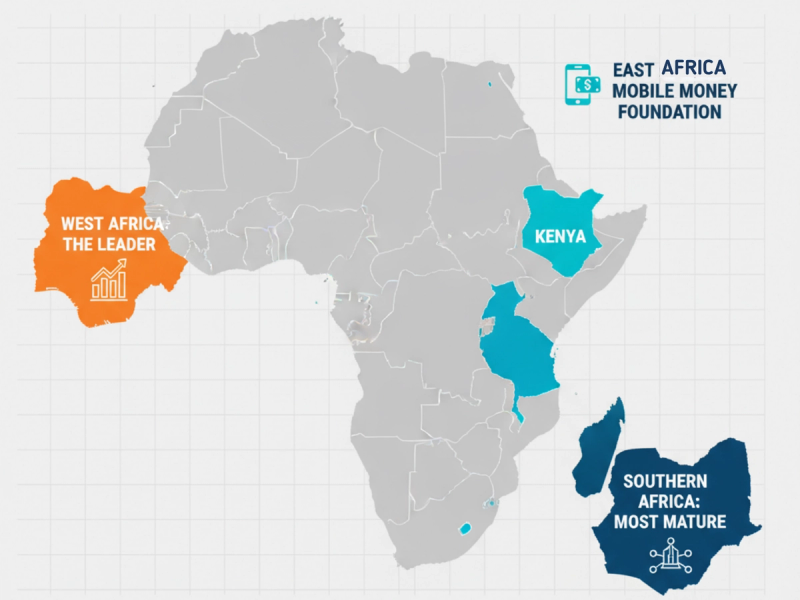

West Africa: Nigeria Leading, Others Following

Nigeria dominates West African embedded finance, accounting for roughly a third of Africa's entire fintech market, according to World Bank analysis. With over 115 million active internet users and 40 million MSMEs, the market opportunity is substantial.

Ghana is developing its embedded finance ecosystem more gradually, with frameworks still evolving. However, several Nigerian platforms are expanding into Ghana, bringing proven models to markets with similar characteristics but earlier-stage adoption.

East Africa: Mobile Money Foundation

East Africa benefits from the region's mobile money infrastructure leadership. M-Pesa's success in Kenya created both consumer comfort with non-bank financial services and a technical foundation for embedded finance to build upon.

Kenya, Rwanda, and Uganda are seeing embedded finance emerge on top of mobile money infrastructure, with payment platforms evolving into comprehensive financial service ecosystems.

Southern Africa: South Africa's Sophistication

South Africa's embedded finance market, valued at $2.63 billion in 2024, represents the continent's most mature implementation. The market benefits from more advanced banking infrastructure, higher smartphone penetration, and sophisticated consumer expectations.

PayJustNow, a South African BNPL provider, now serves 2.5 million users and adds 100,000 customers monthly, demonstrating the scale possible in more developed African markets.

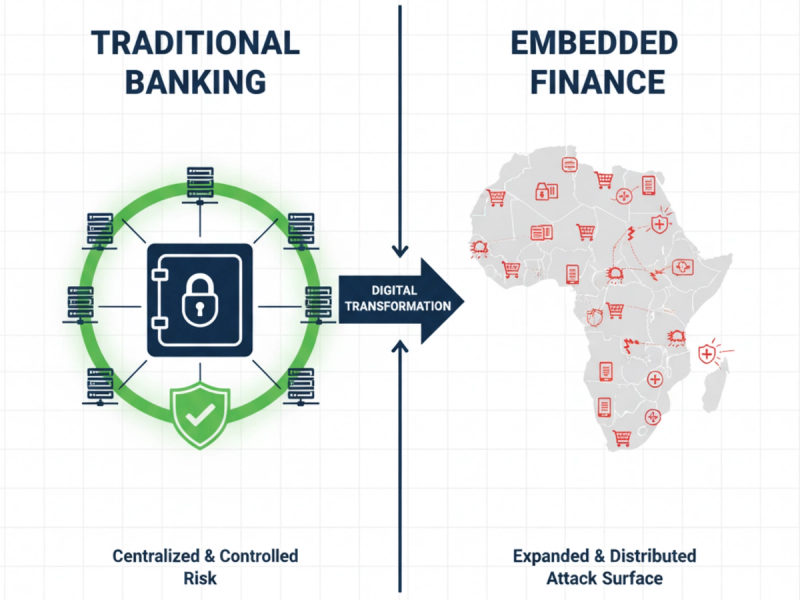

The Risks That Could Limit Growth

Despite impressive growth trajectories, embedded finance in Africa faces several genuine risks that could constrain its potential.

Security

Cyberattacks in Africa rose by 112% in Nigeria between 2019 and 2023, according to Tech In Africa analysis. As embedded finance spreads financial capability across thousands of non-specialized platforms, the attack surface for cybercriminals expands significantly.

A retail platform that embeds lending faces different security challenges than a bank, yet must maintain equivalent security standards. Many platforms lack the security expertise that traditional financial institutions have developed over decades.

Robust encryption and fraud detection systems are critical, but implementation is expensive and technically demanding. This creates a genuine tension between rapid embedded finance expansion and maintaining security standards.

Infrastructure Concentration: The API Risk

A small number of API providers power huge portions of Africa's fintech ecosystem. If a major infrastructure provider experiences significant downtime or security breach, the ripple effects could affect thousands of businesses and millions of consumers simultaneously.

This concentration creates systemic risk. The embedded finance model, where financial services live inside non-financial platforms, multiplies these vulnerabilities across thousands of implementations.

There is an uncomfortable parallel to earlier internet infrastructure: concentration can drive efficiency and standards, but it also creates single points of failure that could have catastrophic consequences.

Regulatory Complexity: Moving Faster Than Rules

Nigeria's regulators, particularly the Central Bank of Nigeria, have laid groundwork with open banking guidelines and rules for payment service providers. The CBN's Payments System Vision 2025 and regulatory sandbox for fintech innovation show progressive regulatory thinking.

However, embedded finance is fundamentally different from traditional fintech. It spreads financial capability across industries, making oversight more complex. A single retail platform may now process as much money as a small financial institution, without looking like one.

The challenge is not hostile regulation but rather regulatory frameworks struggling to keep pace with innovation. When financial services appear embedded in ride-hailing apps, healthcare platforms, and logistics tools, traditional financial regulation frameworks become difficult to apply consistently.

Cost Barriers: The SME Challenge

High implementation costs, ranging from infrastructure to compliance, make it difficult for smaller businesses to adopt embedded finance solutions, according to Tech In Africa research.

SMEs constitute 90% of businesses in Africa, yet many cannot afford the technical integration, compliance requirements, and ongoing operational costs of embedding financial services. Affordable, low-code tools and simplified API integration are essential to reduce entry barriers, but development of these solutions lags demand.

This creates a risk that embedded finance benefits primarily large platforms that can afford sophisticated implementations, potentially increasing rather than reducing inequality in access to advanced financial tools.

Trust: The Invisible Barrier

Perhaps the most significant risk is erosion of trust. As Tech In Africa notes, trust issues persist, especially with the rise of AI-powered services. When financial services are embedded in unfamiliar platforms, consumers may struggle to understand who is providing the service, how their data is protected, and where to seek recourse if problems arise.

Building trust requires time, consistent positive experiences, and strong consumer protection frameworks, all of which are still developing in most African markets.

The Opportunities That Make Risk Worth Taking

Despite genuine risks, embedded finance presents opportunities that could fundamentally improve financial inclusion and economic outcomes across Africa.

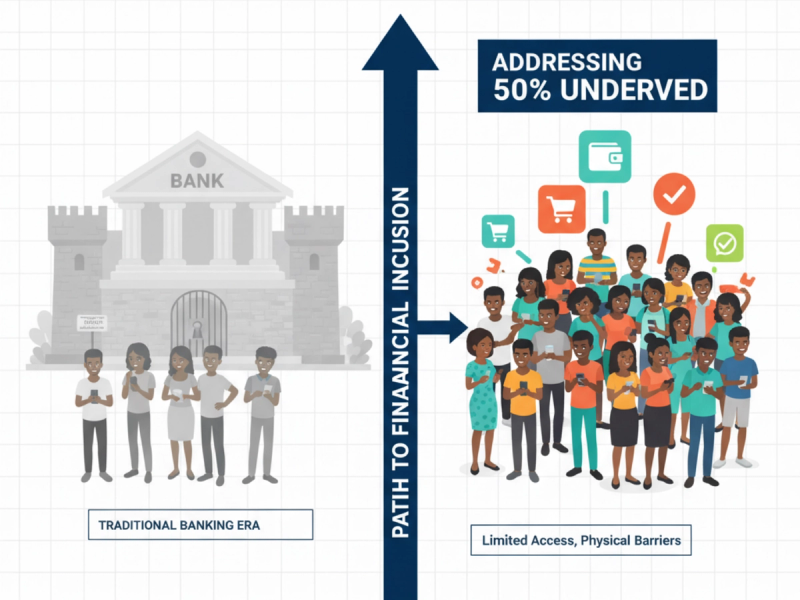

Reaching the Unreached

Embedded finance can extend financial services to populations that traditional banks found economically unviable to serve. By integrating services into platforms people already use, embedded finance eliminates the need for separate bank relationships, physical branches, or standalone financial apps.

With roughly half of Nigeria's adults remaining unbanked or underserved primarily due to limitations of traditional banking infrastructure, embedded finance offers a path to inclusion that doesn't require rebuilding physical banking networks.

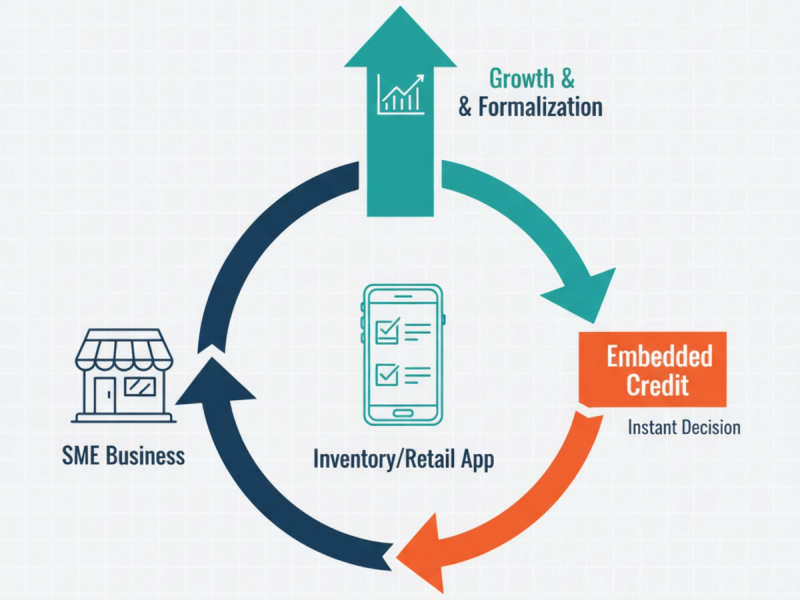

SME Growth Engine

Small and medium enterprises, which constitute 90% of African businesses, could gain significantly from embedded finance. Access to working capital, payment collection tools, business insurance, and investment products, all embedded in the platforms where SMEs already manage their operations, could accelerate business growth and formalization.

Fintech companies are already exploring this opportunity. As one Nigerian embedded finance leader, Faith Ojeiku, notes "Many SMEs struggle to get financing from traditional banks, even though they're running viable businesses", making embedded lending in business platforms particularly valuable.

Cross-Border Opportunity

Cross-border payments represent a transformative application of embedded finance. While platforms like M-Pesa, MTN Mobile Money, and PAPSS are making strides, challenges such as fragmented ecosystems and reliance on vehicle currencies persist.

Embedded finance could make cross-border transactions as seamless as domestic ones by integrating cross-border payment capabilities directly into e-commerce, logistics, and business platforms. This would reduce friction in intra-African trade, which remains surprisingly difficult despite geographic proximity.

Revenue Diversification

For platforms, embedded finance represents significant new revenue streams. According to World Economic Forum analysis, the global embedded finance market is expected to reach $7.2 trillion by 2030, with financial services revenue increasingly flowing to platforms rather than traditional financial institutions.

African platforms that successfully embed financial services can capture portions of this value while improving customer experiences and retention.

The Infrastructure Requirements for Scale

For embedded finance to fulfill its potential in Africa, specific infrastructure investments and developments are necessary.

API Standardization

Fragmented API standards across African markets create unnecessary complexity and cost. Platforms expanding across multiple countries must integrate with different API providers in each market, limiting scale economies.

Regulatory initiatives promoting API standardization, like Kenya's Central Bank guidelines, could reduce integration costs and enable true pan-African embedded finance platforms.

Identity Infrastructure

Robust identity verification remains a fundamental challenge. Embedded finance requires reliable ways to verify customer identities remotely, assess creditworthiness, and prevent fraud, all without the in-person processes that traditional banks use.

At Zeeh, we've built infrastructure specifically to address this challenge, providing real-time identity verification and financial data access across African markets through standardized APIs. This is exactly the type of infrastructure layer that enables embedded finance to scale securely.

Interoperability

For embedded finance to work seamlessly, different platforms and providers must be able to interact. A customer should be able to use embedded banking services from one platform to make embedded payments on another, without friction.

Current African fintech ecosystems remain somewhat siloed, with limited interoperability between different platforms and providers. Solving this requires both technical standards and regulatory frameworks that mandate or incentivize interoperability.

Consumer Protection Frameworks

As financial services spread across thousands of platforms, consumer protection becomes more complex. Clear frameworks defining liability, dispute resolution, and recourse mechanisms are essential for maintaining trust.

This is an area where regulatory development is critical, and where African regulators have the opportunity to create frameworks that other emerging markets could adopt.

What Comes Next: The Three Possible Futures

The trajectory of embedded finance in Africa is not predetermined. Three distinct futures are possible, depending on how key challenges are addressed.

Future 1: Fragmented Growth

In this scenario, embedded finance continues growing rapidly but remains fragmented across countries, platforms, and providers. Each market develops its own standards, regulatory approaches, and dominant players, creating complexity for companies trying to scale across African markets.

This future delivers financial inclusion benefits within individual markets but limits the pan-African impact that fully interoperable embedded finance could provide. It is the path of least resistance, requiring no coordination or standardization, but also the least transformative long-term outcome.

Future 2: Platform Dominance

A small number of large platforms could come to dominate embedded finance, with most integration happening through a handful of infrastructure providers. This future delivers efficiency and user experience benefits but creates concentration risks and potential barriers to entry for new innovators.

Current trends suggest this future is increasingly likely, with Paystack, Flutterwave, and a few others controlling significant market share in key segments.

Future 3: Open Ecosystem

The most promising but most difficult future involves creating truly open, interoperable embedded finance ecosystems where multiple providers can compete on equal terms, platforms of all sizes can integrate financial services, and consumers can move seamlessly between different services.

This future requires coordinated action from regulators, infrastructure providers, and platforms, including standardized APIs, clear regulatory frameworks, robust consumer protections, and investment in shared infrastructure.

The Choice Facing African Markets

The choice ahead is not whether to embrace embedded finance. That decision has already been made by the market. In 2025, embedded financial services are appearing across African commerce, whether regulators, incumbents, or observers are ready for them or not.

The real choice is how to shape this transformation. Will African markets create the regulatory clarity, infrastructure standards, and consumer protections that enable embedded finance to reach its full potential? Or will growth happen in ways that maximize short-term innovation while creating long-term fragmentation and risk?

As one analysis notes, "If embedded finance is supported with the right infrastructure, security frameworks, and regulatory clarity, it can accelerate financial inclusion faster than any standalone bank ever could. If not, it could create blind spots big enough to threaten the stability it helped build."

The signals are clear. Embedded finance is no longer a buzzword whispered in fintech circles. It is already part of the infrastructure that facilitates money movement across African markets. It lives inside apps, platforms, and everyday experiences; quietly, efficiently, and at massive scale.

Policymakers, platform builders, and infrastructure providers now face a strategic moment. The decisions made in 2025 and 2026 about standards, regulations, and infrastructure investments will determine whether Africa's embedded finance revolution fulfills its promise or falls short of its potential.